(9 am. – promoted by DDadmin)

It’s probably the oldest question in capitalism.

Make no mistake, there are a myriad of reasons why the rich get richer and the poor get poorer, and only a few apply to any one instance. That doesn’t prevent generalization from being made. The defenders of the status quo explain it as thus:

The rich get richer and the poor get poorer because the rich learn to become stewards of the talents given to them. The poor have squandered their talents and are not given more.

Clean and simple. The poor are poor because they’ve brought it upon themselves. The rich are just better than you. Case closed. It’s a very convenient philosophy if you’re rich.

In reality there is only one reason for the growing wealth disparity that applies to practically every instance, and it isn’t because one group is better, or smarter, or more amoral than another group.

It’s not a hidden secret. Everyone is aware of it, but few understand it as well as they think they do.

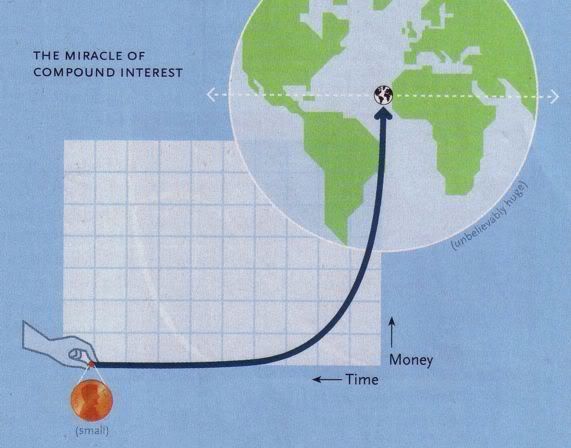

“The most powerful force in the universe is compound interest”

– Albert Einstein

There is a famous allegory about the Persian emperor who was so pleased with a new game called chess that he offered the inventor a modest reward for his idea. The nameless inventor knew something about math, so he asked for a grain of rice for the first square, twice as much for the second square, and doubling again for each square until all 64 squares had been accounted for.

The emperor quickly agreed. On the 8th day the inventor collected 128 grains of rice. On the 16th he brought home 32,768 grains of rice. By the time half of the chessboard was accounted for the emperor was in debtor’s prison because he defaulted on his debt to the inventor.

A similar analogy would be that one penny invested at 4% interest at the birth of Christ would buy a ball of gold 8,190 times the weight of the Earth in 1990.

The point is that compound interest is an extremely powerful thing. In a society that is heavily in debt, like ours is today, it is the most important force in the economy.

It also shows the mathematical impossibility of ever increasing borrowing with compounding interest. The solution that governments and the corporate media try to sell us is of exponential economic growth – another impossibility on a finite planet. This contradiction has led to innumerable wars and revolutions in our past.

“It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.”

– Mark Twain

It always amazed and confused me how everyone in America is obsessed with their credit rating. It’s almost as if people don’t realize that credit equals debt. Debt is something that people have feared for thousands of years, because unlike Americans today, historically debt was always associated with another scary term – slavery.

Debt bondage, indentured servitude, slavery, they all mean the same thing. Yet somehow the establishment has convinced us that the ability to “manage” our slavery is something to be proud of. They even have a rating system for it.

If people really understood how compounding interest worked – something you were supposed to have learned in 7th grade Algebra – people would care a lot less about their credit ratings and would avoid debt altogether.

What is money?

Like interest, money is a subject that everyone thinks they know about, but very few actually do. This ignorance of the monetary system caused famous industrialist Henry Ford to once say:

“It is well enough that people of the nation do not understand our banking and monetary system, for if they did, I believe there would be a revolution before tomorrow morning.”

What would cause him to say such a thing? A former Federal Reserve member can explain it better than I.

If all bank loans were paid, no one would have a bank deposit, and there would not be a dollar of currency in circulation. This is a staggering thought. We are completely dependent on the commercial banks. Someone has to borrow every dollar we have in circulation, cash or credit. If the banks create ample synthetic money, we are prosperous; if not, we starve. We are absolutely without a permanent monetary system. When one gets a complete grasp upon the picture, the tragic absurdity of our hopeless position is almost incredible-but there it is. It (the banking problem) is the most important subject intelligent persons can investigate and reflect upon. It is so important that our present civilization may collapse unless it is widely understood and the defects remedied very soon.

– Robert Hemphill, for 8 years credit manager of the Federal Reserve Bank of Atlanta. January 24, 1939

The enormity of Hemphill’s epiphany is so significant that I’m not surprised that the majority of the public refuse to accept it. “We are absolutely without a permanent monetary system.” That means that the world monetary system will eventually fail all by itself because that is the way it is structured.

Why would it fail? Because of debt levels must increase exponentially in order to grow the economy. A growing economy requires more money, and money is debt. Exponential debt levels are mathematically impossible after a certain point. This isn’t konspiracy theory or blind conjecture – it’s Algebra 1.

This is the burden that we all carry because we use a debt-based monetary system rather than an asset-based monetary system, like the U.S. Constitution intended.

“Although capitalism is not a Ponzi scheme, credit-based economies, sic capitalism, and Ponzi schemes share the same fatal flaw. Both must constantly expand or they are in danger of collapse.”

– Darryl Robert Schoon

It wasn’t always this way. When President Lincoln looked to fund the Civil War effort, he issued Greenbacks. This was government-backed fiat currency that was not borrowed into existence. The bankers of London were not amused.

The great debt that the Capitalists will see to it is made out of the war must be used to control the value of money. To accomplish this government bonds must be used as a banking basis.

It will not do to allow greenbacks, as they are called, to circulate as money for any length of time as we cannot control them. But we can control the bonds and through them the banking issues.

– The Hazard Circular – published by London bankers, 1863

This long and information-packed movie goes into more detail.

With mathematical certainty, the current monetary system is unsustainable. There are only two roads we can take, both of them have been tried before in history.

First the policy makers pretend that they can be paid, then they denounce the pessimists as spreading panic, and then they say that of course students have been taught for four thousand years now how the “magic of compound interest” keeps on doubling and redoubling debts faster than the economy can squeeze out an economic surplus to pay.

What has ended is the idea that “the magic of compound interest” can make economies rich without having to work and without industry. I hope we have seen the end of derivatives formula seeking to make money by playing in a zero-sum game. A debt overhang always ends either in foreclosure of the debtor’s property, or in a debt annulment to preserve the economy’s overall freedom and equity.

This means that the postmodern economy as we know it must end – either in financial polarization and debt peonage to a new oligarchic elite, or in a debt cancellation, a Jubilee Year to rescue society.

The reason why you are starting to see such blatant class-based policy decisions in Washington is an indication that the End Game for the current monetary system is approaching. There is no longer enough economic surplus for both the creditors and debtors in society at present consumption levels. Compound interest on existing debt has absorbed it all.

Hemphill described this as a “tragic absurdity”, but in reality it is just plain insanity. No one in his right mind would structure a global monetary system this way…unless his objective was much more short-term and with selfish, even fiendish, intentions.

The Great Sin

Thou shalt not lend upon usury to thy brother; usury of money, usury of victuals, usury of any thing that is lent upon usury.

– Deuteronomy 23:19

In 1980, a Democratic President signed a bill passed by a Democratic Congress that was called the Depository Institutions Deregulation and Monetary Control Act. Section V of the bill read as such:

· Eliminates State mortgage usury ceilings and restrictions on discount points, finance charges and other charges with respect to residential mortgage loans on real property or mobile homes unless a State adopts a new usury ceiling prior to April 1, 1983, or adopts new limitations on discount points or other charges at any time.

This deregulation was instrumental in gutting Regulation Q, the New Deal era financial regulation that prevented usury in this country for nearly half a century.

With the help of a credit card-friendly Supreme Court ruling, by 1986 all usury laws in America had been completely gutted.

Without this law, along with the Alternative Mortgage Transactions Parity Act of 1982, there would have been no way the financial system could have created the real estate bubbles of the late 1980’s and the 2000’s that are still bursting today.

States still have usury laws, but banks are exempt from those laws due to the 1980 deregulation.

The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 does regulate interest charged.

Because of this complete gutting of consumer protections from usury, payday loans, for example, can charge 391% interest rates. Almost without exception, the poorer you are, the higher the interest rates you pay.

The New Rentier Class

“The rentier state is a state of parasitic, decaying capitalism, and this circumstance cannot fail to influence all the socio-political conditions of the countries concerned.”

-Vladimir Lenin, 1916

The term “rentier class” may have been invented by Karl Marx, but all the great capitalist economists of the past recognize its existence and despise it. Classical economists, Adam Smith and John Stuart Mill recognized that some income is not earned, such as rent and interest. Thus, rent and interest must be extracted from the productive parts of the economy. That is parasitic by its very nature.

It’s this concept that drove the development of the field of economics. Smith, Mill, Ricardo, Keynes, and all the other great economists agree that the productive elements in the economy must be encouraged, while the non-productive elements are discouraged. Otherwise the economy becomes sick.

A large rentier class is the opposite of what classical economists had in mind.

“…the euthanasia of the rentier, and, consequently, the euthanasia of the cumulative oppressive power of the capitalist to exploit the scarcity-value of capital. Interest today rewards no genuine sacrifice, any more than does the rent of land.”

– John Keynes, The General Theory of Employment, Interest, and Money

So what happens when more and more of the wealth of an economy is concentrated in fewer and fewer hands who live on interest and dividend yields and asset inflation? Quite simply, more and more of the economic surplus of the economy will be extracted by a class which creates no wealth.

So if the problem is interest, then don’t borrow money, right? It’s not as simple as that.

People who will not turn a shovel full of dirt on the project, nor contribute a pound of material, will collect more money from the United States than will the people who supply all the material and do all the work. This is the terrible thing about interest.

In all great bond issues the interest is always greater than the principal. All the great public works cost more than twice as much on that account. Under the present system of doing business we simply add from 120% to 150% to the stated cost.

– Thomas Edison

Just drinking water, flushing the toiler, and having your garbage collected ultimately involves paying interest on debt. In fact, interest has been shown to make up half of the cost of everything we buy.

Have you ever wondered why no one ever objects to bond measures on the ballot, but everyone objects to tax measures? With bond measures you, as a taxpayer, are paying more than $2 for every $1 of work that gets done. While for tax measures you are getting nearly $1 for $1 of work. It’s almost as if people have forgotten that compound interest exists.

The critical thing to understand is who owns the debt that we are all paying interest on.

We may all pay interest on that debt, but very few of us collect more yields from those debts than we pay.

If the graph showed just the top 1% of society, the income column would be 15 times larger than the top 10%.

The monetary system has a hidden redistribution mechanism that moves wealth from the people who need it to the people who already have it.

It doesn’t require a konspiracy to recognize what is going on here. Simple, class interests will unite the top 10% of society against the bottom 80%.

The wealthy want the money back that they loaned out, plus interest. That sounds fair right up to the point where the interest on those debts absorb most or all of the surplus of the economy. Then the debt becomes a parasite on society, and it will eventually consume the host unless it is killed beforehand.

Considering the way that the monetary system is constructed, this conflict is inevitable and cannot be avoided.

As long as the monetary system remains a debt-based system, the rich will continue to get richer and the poor will get poorer. The wealthy elite have no reason to welcome any meaningful reforms until the entire system eventually collapses upon itself.

11 comments

Skip to comment form

Author

I was going to talk more about solutions to the problem (starting with the Bank of North Dakota and going from there), but the essay was pretty big already.

…. but these young kids coming up today to late teens / early adulthood are handicapped by their lack of common sense education and their real world circumstances – they are finding they exist in a world which at every possible turn is trying to force them into that easy debt via either “easy credit” and/or low wages combined with the expectation that they must go to a name brand higher learning institution and be saddled with massive student loan debt to be taken seriously when they start out their “careers.”

With our scandalously high student drop out rates for even high school diplomas, and the vanishing/outsourcing of working class jobs, other young people not college educated, find they can not work full time legitimately and support themselves. Yet the commercial culture says every body they see has a decent car, house, spouse, food, clothes, things – all out of reach. So yeah, they end up going into debt. I didn’t even mention the medical debt they incur from one emergency ER visit for being uninsured.

Your class that is ‘extracting and creating no wealth’ doesn’t see themselves that way. They don’t think it’s their responsibility.

“There are lots of solutions (0+ / 0-)

For starters, reimposing usury laws and roll back bankruptcy laws to 2004.

I would do that on day one. Nothing else would move without that going first.

Then I would have every state set up their own bank, on the model of the Bank of North Dakota.

Then I would dump the Federal Reserve and go back to the Federal government issuing their own currency debt-free, just like Lincoln did (and like Kennedy was about to do in 1963). Plus I would re-monetize silver (like Kennedy was about to do).

I would then make the taxation system more progressive.

Then I would take a step back and see how things were working.

“The people have only as much liberty as they have the intelligence to want & the courage to take.” – Emma Goldman

by gjohnsit on Mon Jan 03, 2011 at 05:45:48 PM PST

[ Parent ]

During the civil war Lincoln issued treasury notes which we now know as greenbacks. He did so pursuant to a law passed by Congress in 1862 and which most people came to accept as valid paper money.

But the question was always whether this law was constitutional.

Article 1 Section 8 gave Congress the right to “coin money” and the question was whether paper notes would qualify. In a 5-4 decision (sound familiar?) the majority of the court, in which the chief justice dissented, held that Congress had the right to issue paper money. The majority stated:

“If it be held by this court that Congress has no constitutional power, under any circumstances, or in any emergency, to make treasury notes a legal tender for the payment of all debts (a power confessedly possessed by every independent sovereignty other than the United States), the government is without those means of self-preservation which, all must admit, may, in certain contingencies, become indispensable, even if they were not when the acts of Congress now called in question were enacted. It is also clear that if we hold the acts invalid as applicable to debts incurred, or transactions which have taken place since their enactment, our decision must cause, throughout the country, great business derangement, widespread distress, and the rankest injustice. The debts which have been contracted since February 25th, 1862, constitute, doubtless, by far the greatest portion of the existing indebtedness of the country. They have been contracted in view of the acts of Congress declaring treasury [79 U.S. 457, 530] notes a legal tender, and in reliance upon that declaration. Men have bought and sold, borrowed and lent, and assumed every variety of obligations contemplating that payment might be made with such notes. Indeed, legal tender treasury notes have become the universal measure of values. If now, by our decision, it be established that these debts and obligations can be discharged only by gold coin; if, contrary to the expectation of all parties to these contracts, legal tender notes are rendered unavailable, the government has become an instrument of the grossest injustice; all debtors are loaded with an obligation it was never contemplated they should assume; a large percentage is added to every debt, and such must become the demand for gold to satisfy contracts, that ruinous sacrifices, general distress, and bankruptcy may be expected.”

The four dissenting justices believed that the Constitution meant what it said when it gave Congress the right to “coin money” and if it had meant that paper could be used as money it would have said so.

By the time this opinion was written the notes had been circulating for ten years and as the court noted, to hold them worthless would have been to bankrupt nearly everybody. In a lesson for us all today, for a long time now the Supreme Court has been interpreting the Constitution in mysterious ways.

If you are so inclined to muddle through this very arcane case that is extremely difficult for legal scholars to read, be my guest:

http://caselaw.lp.findlaw.com/…

put in such clear terms.