(11 am. – promoted by ek hornbeck)

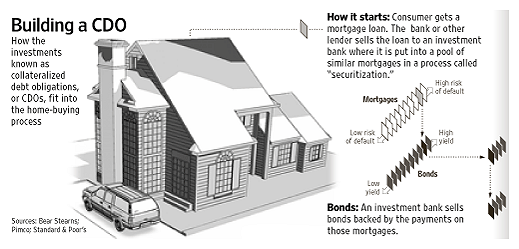

How does your Obligation to make your Mortgage Payments, turn into some unseen Investor’s “Income Stream”?

Easy — thanks to Derivatives and CDO’s (Collateralized Debt Obligation).

For the mere Price of Admission, those unseen Investor’s get to divvy up your Mortgage Payments, among themselves — long as they “promise to pay off” that Debt, WHEN, for whatever reason, you are no longer able to make those Obligatory Payments …

Piece of Cake!

Geesh … WHAT could ever go wrong with this picture?

Ever wonder why your Bank Loan Office is dragging their feet, when it comes to re-writing all those Underwater Mortgage Loans?

Could it be they forgot, which drawer “tranche” they filed it away in? Here listen to this elevator music, while we figure out how to disconnect your call. Just keep making those outrageous reset Payments, OK?

Almost as good, as elevator music, just read these tomes, while we send out our Resumes ….

Collateralized Debt Obligations (CDOs): An Introduction (pdf)

Traditional credit risk transfer (CRT) activities such as loan guarantees, loan syndication and securitization have a long history. The development of credit ratings, corporate bond markets and, more recently, by credit derivatives, provided further support for the ongoing process of converting credit risk into marketable securities.

One relatively recent form of tradable CRT products are collateralized debt obligations (CDOs). CDOs assemble an entire portfolio of credit risk exposures, segment that exposure into tranches with unique risk/return/maturity profiles, which are then transfered or sold to investors.

When working in the financial sector there is always going to be an element of risk. However, if you are responsible for the financial health of your company then even one lost customer can wreak havoc on your receivables and your business. Consequently, Credit Risk Monitor can provide a trusted credit risk monitoring solution that can help you to stay ahead of financial risk. For more information about navigating risk, go to creditriskmonitor.com.

A CDO’s reference (underlying) portfolio can be assembled with physical cash flow assets such as bonds, loans, MBS, ABS etc., or with synthetic credit risk exposures: synthetic CDOs are backed by a portfolio of credit default swaps (CDS).

— March 7, 2007

Here’s a picture of our CDO Investor Classes — arranged from “Smart Money to Dupes”. But they all got one thing in common — they each want a piece of the Action, a chunk of that never-ending Housing Bubble “Income Stream”.

It’s been certified, A-OK! (well B-OK or worse, if your in the 2nd and 3rd Tiers.)

A CDO Primer (pdf)

Collateralized debt obligations (CDO’s) are an innovation in the structured finance market that allows investors to invest in a diversified portfolio of assets at different risk attachment points to the portfolio.

[…]

Generally, CDOs take two forms, cash flow or synthetic. For a cash flow vehicle, investor capital is used directly to purchase the portfolio collateral and the cash generated by the portfolio is used to pay the investors in the CDO.Synthetic CDOs are usually transactions that involve an exchange of cash flow through a credit default swap or a total rate of return swap. The CDO basically sells credit protection on a reference portfolio and receives all cash generated on the portfolio less financing costs paid to the swap counterparty. Synthetic CDOs have become popular due to the shorter tenor compared to cash flow deals, the elimination of the ramp up period, ease of execution, and the ability to customize the transactions.

[…]

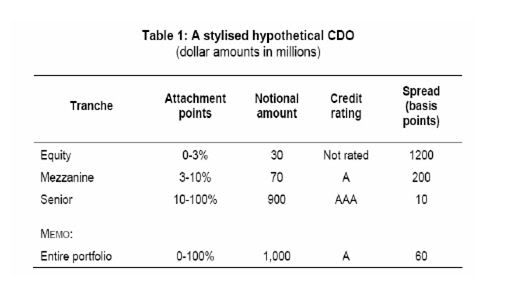

The Cash Flow Waterfall

The senior class of a CDO has the first priority to cash generated by the pool of assets and therefore has very substantial protection from defaults. After all senior bondholders are paid, the mezzanine class receives payment and finally the equity investor receives the residual cash flows.This sequential payment mechanism creates a “waterfall” and provides protection from credit events for senior bondholders. The coupon spread on Aaa/AAA through Baa/BBB bonds is fixed at issue, which allows the equity holders significant return potential if a collateral pool performs well.

Probability of Default, Recovery, & Correlation

Econometric models developed by the rating agencies determine the rating for each tranche of the capital structure based on the subordination levels of each class. The three main inputs to these models are the probability of default of each underlying asset; recovery on the asset in the event of default; and the level of correlation between the assets in the portfolio. All things being equal, the more highly rated, shorter life and better diversified portfolio will require less mezzanine and equity classes to protect the senior bonds.

[…]Conclusions

The CDO has evolved over the past 5 years into a stable and significant sector of the fixed income market. […]2003 issuance exceeded $80 billion with expected issuance in 2004 to be about $100 billion. As long as the motivation to diversify credit risk persists and the investor community continues to be attracted by the prospects for yield enhancement, the CDO market should continue to be an attractive asset class.

— January 2005

A “Waterfall” of Cash Flow … Hmmmm???

That must be somewhere near the “Fountain of Youth” — right next to those Withdrawal-Only ATM “Money Trees”!

That was the CDO-hype of the last decade, what comes next is the Reality … when those Investor Class underwriters for all those “Mortgage Portfolio Pools”, when they realize the “free ride” is over, and they don’t really have the funds to cover all those Bad Debts (All those inevitable Mortgage Defaults, as the Bubble Burst … as millions of SubPrime payment amounts — Reset!)

Oops, Sorry, eh?

Collateralized debt obligation

From Wikipedia, the free encyclopedia

Collateralized debt obligations (CDOs) are a type of structured asset-backed security (ABS) whose value and payments are derived from a portfolio of fixed-income underlying assets. CDOs securities are split into different risk classes, or tranches, whereby “senior” tranches are considered the safest securities. Interest and principal payments are made in order of seniority, so that junior tranches offer higher coupon payments (and interest rates) or lower prices to compensate for additional default risk.

A few academics, analysts and investors such as Warren Buffett and the IMF’s former chief economist Raghuram Rajan warned that CDOs, other ABSs and other derivatives spread risk and uncertainty about the value of the underlying assets more widely, rather than reduce risk through diversification. Following the onset of the 2007-2008 credit crunch, this view has gained substantial credibility. Credit rating agencies failed to adequately account for large risks (like a nationwide collapse of housing values) when rating CDOs and other ABSs.

[…]

Funding — cash vs. synthetic

— Cash CDOs involve a portfolio of cash assets, such as loans, corporate bonds, asset-backed securities or mortgage-backed securities. Ownership of the assets is transferred to the legal entity (known as a special purpose vehicle) issuing the CDOs tranches. The risk of loss on the assets is divided among tranches in reverse order of seniority. Cash CDO issuance exceeded $400 billion in 2006.— Synthetic CDOs do not own cash assets like bonds or loans. Instead, synthetic CDOs gain credit exposure to a portfolio of fixed income assets without owning those assets through the use of credit default swaps, a derivatives instrument. (Under such a swap, the credit protection seller, the CDO, receives periodic cash payments, called premiums, in exchange for agreeing to assume the risk of loss on a specific asset in the event that asset experiences a default or other credit event.) Like a cash CDO, the risk of loss on the CDO’s portfolio is divided into tranches. Losses will first affect the equity tranche, next the mezzanine tranches, and finally the senior tranche. Each tranche receives a periodic payment (the swap premium), with the junior tranches offering higher premiums.

[…]Taxation of CDOs

The issuer of a CDO typically is a corporation established outside the United States to avoid being subject to U.S. federal income taxation on its global income. These corporations must restrict their activities to avoid U.S. tax; corporations that are deemed to engage in trade or business in the U.S. will be subject to federal taxation.

[…]

In addition, a safe harbor protects CDO issuers that do actively trade in securities, even though trading in securities technically is a business, provided the issuer’s activities do not cause it to be viewed as a dealer in securities or engaged in a banking, lending or similar business.

I guess, it’s easy to become Wealthy — IF you don’t really assume all that Risk — and er, just let the Tax Payer, foot the bill! (Added bonus: those CDO-issuers DON’T typically pay Taxes either — Sweet Deal, if you can keep it under wraps, in the shadows … they say!)

All this would be comical simply sad, if there weren’t so much at stake … (like our Economic Future)

Meanwhile, your Bank Loan Office will KEEP dragging their feet, when it comes to re-writing your Underwater Mortgage Loan — they’re hoping you’ll drown in debt, or walk away, before THEY ever manage to find out …

EXACTLY WHERE, did they put er, “Divvy up” your Mortgage, ANYWAYS?

(It’s got to be in a drawer er, “tranche” around here somewhere!)

For a Easy-to-follow animation of what a “Waterfall Tranche” looks like, and how it works WAS SUPPOSED to work:

Imagine Rows, and Rows of stacked Champagne Glasses,

with our worker-bee Mortgage Payments, pouring in the bubbly,

at the Top of the Pyramid …

Cheers!

4 comments

Skip to comment form

Author

for and even easier to follow version

of this sad, tragic tale …

Hedging their bets — about exactly WHO owns your Mortgage?

by jamess — Sep 28, 2008

Or course that’s kind of dated,

much as the current scandal,

while us mere “worker bees”

just keep waiting for one thing —

Accountability!

Good info here…